Finance

Finance’s Ongoing Digital Transformation

Published : 6 years ago, on

Ian Waters, Director, Solutions Marketing, ThousandEyes

With an estimated 20 million people in the UK logging into a banking app per month, it would seem that the ‘digitisation’ of the finance sector has really started to take off. This is especially welcome for the industry now as a number of financial organisations in the UK have announced plans to close bricks and mortar bank branches across the country for good.

However, when the China Construction Bank launched its fully automated, human-free bank branch this year, it pointed to how the banking experience, regardless of in-branch or online, may look in the future.

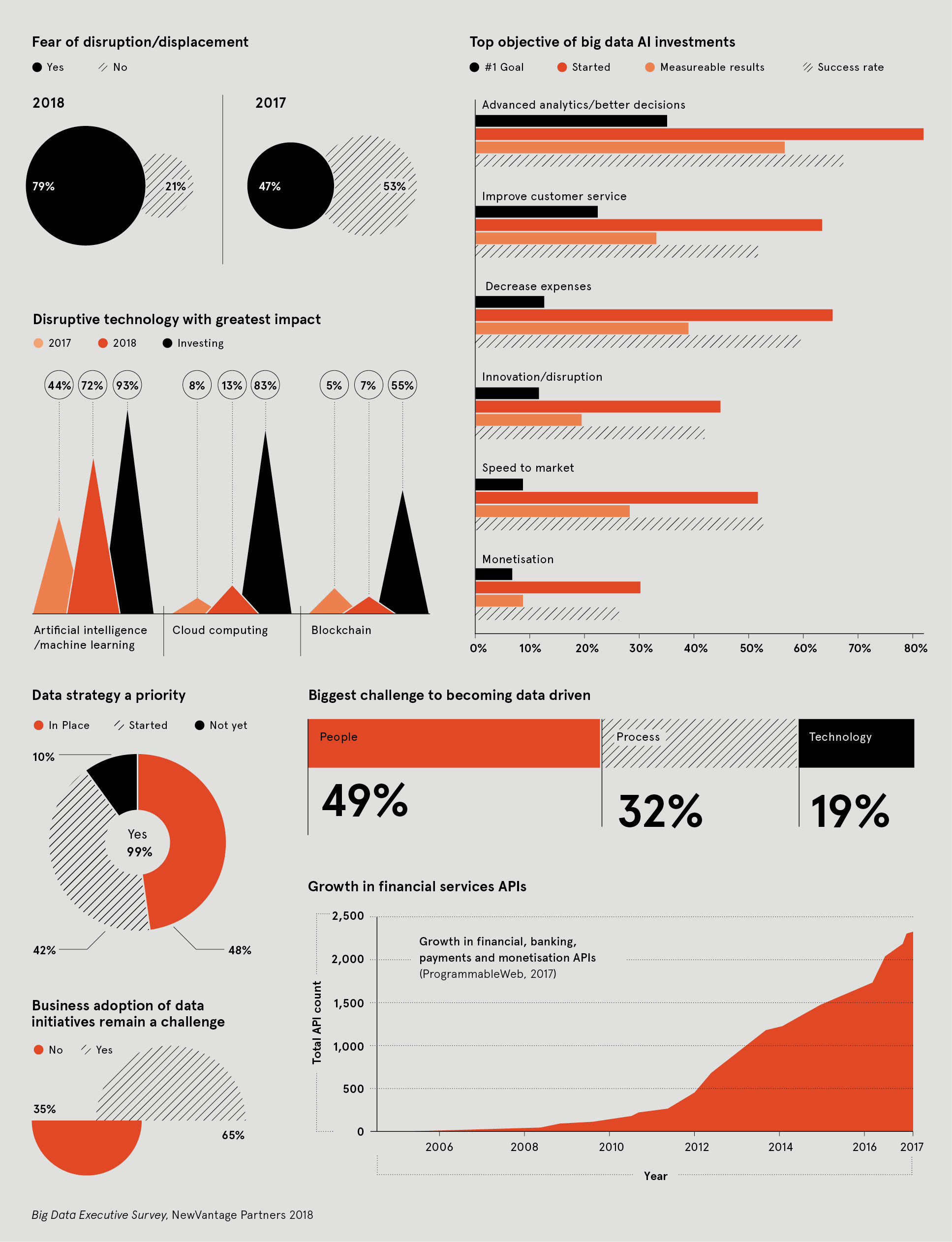

The truth is that whether it is in-branch or online, the digital transformation of the sector is a reality that is affecting banks profoundly. In fact, 79% of financial sector professionals admit they fear financial disruption, in light of the rise in ‘challenger’ bank offerings. For example, it is currently estimated that over 1,600 fintech companies are currently operating in the UK. Thanks to these newcomers to the industry, consumers’ long standing expectations of banking have actually been deeply challenged, leading to an increased demand for innovative, technology-focused services. In today’s banking, end users are demanding speedy, personalised, and coordinated banking services, across all channels. Due to this situation, banks are currently undergoing huge digital transformations to keep pace with these new challengers.

Banking ‘digital transformation’ is the omni-channel integration of digital technologies for the financial services customer experience. The reason why it matters so much today is because it seeks to deliver a seamless customer experience that could begin across any channel. Be it a bank’s website or mobile app, this can help a consumer to enhance their experience in a physical branch.

For example, Santander has created an in-branch experience whereby the space is designed to specifically orientate its customers toward digital touch points, such as interactive touchscreens. Meanwhile, Fidor Bank, a branchless, digital-only ‘challenger’, enables new customers to complete a quick video identification process on a mobile device to sign up in a speedy manner.

What these in-branch and online innovations in customer experience points to is how crucial responsiveness, reliability and speed are to digitisation in banking. It is easy to see why traditional retail banks are pushing for digital transformation, the UK market is now filled with fast growing challengers, while digitisation can help them to achieve a 20% increase in revenues and a 30% decline in expenditures.

However, underpinning this ever-evolving banking experience is an IT infrastructure and network that is extremely complex. Importantly too, the majority of banks are now relying on 3rd parties to deliver a lot of their IT infrastructure, often meaning their own IT teams do not have direct access or control. These third-party providers now have an integral role in the digital banking experience, delivering services ranging from internet and branch connectivity, to software and infrastructure-as-a-Service (SaaS & IaaS), or content delivery (CDN) and security (DDoS Mitigation). In addition, a modern web app normally has numerous third party components, which are accessed via Application Programming Interfaces (APIs), all of which are required to function for the banking experience to be anyway successful. If any part of this mosaic crumbles, regardless of the reason, potential customers, be they in-branch or online could potentially lose access to specific websites and integrated services.

As digitisation grows at a breathtaking pace, IT infrastructure is becoming all encompassing, which has resulted in banks being blind to their entire digital supply chain that currently runs across the Internet. Crucially this means that if there is an outage, they may not be able to quickly understand how it happened, or even where. Outside of this, a newer trend called ‘multi-cloud’ has also arisen for banks. This refers to their digitised operations increasingly being across a number of different cloud platforms. For example, a Gartner report, has predicted that organisations who have a digital strategy focusing on multiple IaaS and PaaS providers will become the most common approach for enterprises by 2019. In the age of cloud-based, agile services, traditional strategies for gaining visibility over entire IT operations can no longer work.

This is why, for the banking industry, ‘Network Intelligence’ is already playing an essential role, helping banks to see exactly where something has gone wrong, like an outage, but also to act quickly to deal with it. It refers to a modern approach to managing today’s ever expanding IT network. It provides end-to-end visibility across all of a retailer’s networks and connected devices that they rely heavily on. Given the amount of money at stake in financial services, this type of reactiveness is essential to reassure customers.

Network Intelligence leverages a unique dataset that captures network topologies, dependencies, and behavior from an unmatched distribution of vantage points that exist throughout the Internet, within the bank’s organisation, and on end-user devices, and, in addition, includes collective data from other Internet-centric organisations. It then employs innovative algorithms to sort through this global dataset and surface issues via an intuitive interface that enables retailers to manage every network like it’s their own. What this all adds up to is that Network Intelligence arms every retailer, and their IT support, with an accurate, up-to-the-moment understanding of what’s happening in the network, both inside and outside of their companies.

Overall, the digitisation of the banking industry has the potential to transform the entire sector for generations to come, as well as enable organisations to their cut costs, and reduce time to market new, innovative products. However, the simple fact is that IT infrastructure is getting more and more intricate and as digitisation continues to grow exponentially, and the ‘bank of the future’ looms, financial organisations have to be able to manage any potential IT outages. With the rapid advancement in network monitoring and intelligence, this challenge can be faced up to and overcome right now, and also importantly, in the future, regardless of how financial services will look.

-

Finance3 days ago

Finance3 days agoPhantom Wallet Integrates Sui

-

Banking4 days ago

Banking4 days agoGlobal billionaire wealth leaps, fueled by US gains, UBS says

-

Finance3 days ago

UK firms flag over $1.4 billion in labour costs from increase in national insurance, wages

-

Banking4 days ago

Italy and African Development Bank sign $420 million co-financing deal

{kind=link}